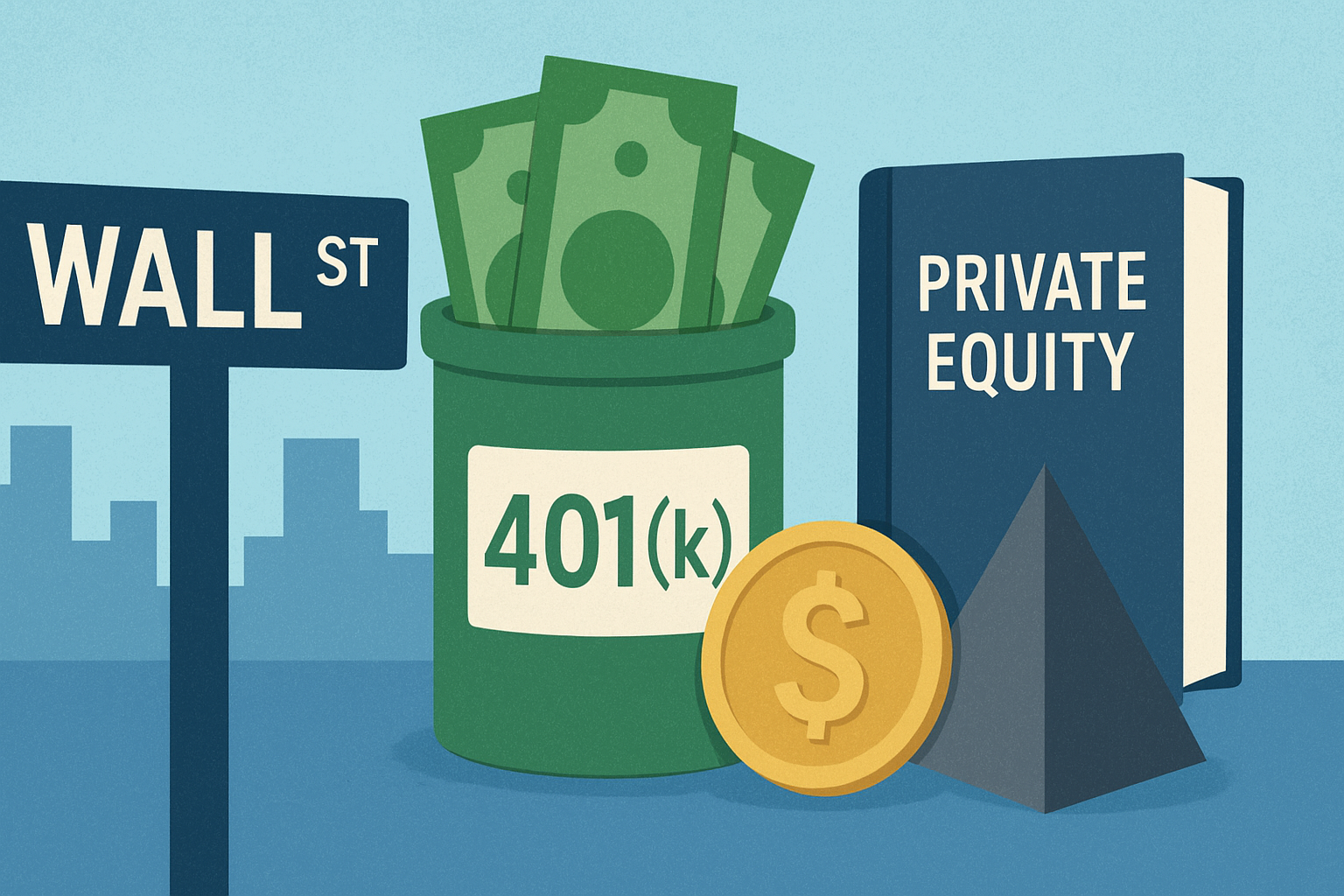

In a move that could reshape the retirement savings landscape for millions of Americans, President Donald Trump has signed an executive order directing regulators to open the door for 401(k) plans to include private market investments. The order, signed on August 7, 2025, instructs the Department of Labor (DOL), Securities and Exchange Commission (SEC), and Treasury Department to update regulations and guidance to allow broader access to private equity, real estate, hedge funds, infrastructure projects, and even cryptocurrency within defined-contribution plans.

The change builds on a 2020 DOL bulletin that cautiously permitted private equity exposure within professionally managed retirement funds but stopped short of allowing them as stand-alone options. The new directive goes significantly further, aiming to normalize alternative investments in retirement accounts and reduce legal uncertainty for employers and plan fiduciaries who include them.

Supporters of the order argue that the move will “democratize” access to asset classes historically reserved for institutional investors and the wealthy. Proponents say private markets often deliver higher long-term returns, fueled in part by the so-called “illiquidity premium.” Large asset managers—including BlackRock, Apollo, and Vanguard—are reportedly developing new target-date and balanced funds designed to incorporate private market allocations in a way that could be digestible for average investors.

However, the plan has sparked significant caution from regulators, financial planners, and consumer advocates. Critics point to the high fee structures typical in private equity—often a “2 and 20” model, meaning a 2% annual management fee plus 20% of profits—compared with the low-cost index funds that dominate many retirement portfolios today. They also highlight the lack of liquidity, limited transparency in pricing, and the complexity of valuing private assets, which are not traded on public exchanges.

The DOL has previously warned that most 401(k) plan sponsors, especially smaller employers, may lack the expertise needed to prudently assess and monitor such investments. Without careful oversight, they say, participants could face outsized risks. Consumer advocates fear that workers nearing retirement could see their savings exposed to volatile or illiquid holdings just when they most need stability.

Despite the concerns, the executive order has energized private equity firms, crypto fund managers, and alternative asset providers, who view the 401(k) market—home to roughly $7.3 trillion in assets—as a massive growth opportunity. Industry groups have already begun lobbying for clear rules to limit fiduciary liability and promote education for plan participants.

Next steps will include formal rulemaking by the DOL, SEC, and Treasury, which will determine how these investments can be offered and what safeguards must be in place. Analysts expect initial products to appear in the form of diversified, professionally managed vehicles rather than direct participant investments into single private market funds.

Whether this change will lead to higher returns for savers or introduce new risks into retirement portfolios will likely depend on the execution. As regulators, asset managers, and employers navigate the shift, millions of Americans could soon find their 401(k) menus offering options once reserved for Wall Street insiders—a development that could transform both the opportunities and the dangers in retirement investing.

Leave feedback about this

You must be logged in to post a comment.